Rule 4 Deductions on Each-Way Bets

Loading...

Rule 4 is the only deduction that quietly trims your each-way return

The first time Rule 4 took 25p in the pound off my return on a 12/1 each-way slip, I genuinely thought the bookmaker had made a mistake. I had won. The horse had placed. The price was the price. Why was my £35 place return suddenly £26? The man behind the counter pointed to a card pinned to the wall — the Tattersalls deduction scale, printed in red and black, a list of pence-in-the-pound figures next to a list of fractional odds. A horse had been withdrawn at 5/2 that morning. Rule 4 had taken 25p in the pound from every winning bet on the race. There was no mistake. I had just never read the small print.

Tom Segal of Racing Post — the racing journalism’s longest-running tipping column under the Pricewise byline — wrote the line I keep coming back to on this point, paraphrased rather than quoted because it sums up an honest market reality: in any year where the major UK firms make money on a Saturday handicap, Rule 4 has done a quiet share of the work. The scale itself has not changed in decades. It is the same Tattersalls Rule 4(c) deduction that has applied to UK fixed-odds settlements since the post-war rebuild of the off-course betting market. What has changed is the rate at which late withdrawals trigger it. Affordability checks have driven smaller fields and twitchier trainers; horses are pulled out closer to the off than they used to be, and Rule 4 fires more often as a result.

The point of this article is that Rule 4 hits both legs of an each-way bet. Most punters know the win leg takes the cut. Not all of them know the place leg does too. The same percentage deduction comes off both, and on a longer-priced runner that is enough money to notice.

How Rule 4 actually works

The rule fires when a horse is withdrawn from a race after the betting market has opened but before the race goes off — late enough that the bookmaker has already accepted bets at prices that assumed the horse was running. The withdrawn horse’s price at the moment of withdrawal determines the deduction rate, and the deduction is applied to every other runner’s winning bet on the race in question. The deduction is taken from the gross winnings, not from the stake — so your stake comes back in full, and the price you took is just rolled back by the deduction percentage.

The scale lives in the Tattersalls Rules of Betting and is the same at every UK-licensed operator. A withdrawn favourite at, say, 4/9 or shorter triggers a deduction of 90p in the pound, the maximum on the scale. A withdrawn outsider at 25/1 or longer triggers no deduction at all. Between those extremes, the scale climbs in steps: 5p at 11/4-3/1, 10p at 9/4-5/2, 15p at 7/4-2/1, 20p at 7/4 shorter, and so on. The exact step bands are published in every operator’s rulebook and are the same across the industry by convention.

Crucially, the deduction applies to the price you took, not to the current market price. So if you took 12/1 about a horse on Friday evening, and a 5/2 favourite is withdrawn on Saturday morning before the race, your slip is settled at 12/1 less 25p in the pound — effectively 75% of 12/1. That is the calculation the till performs at settlement. The bookmaker is not repricing your bet; they are applying a market-wide deduction to compensate for the price-shortening effect of the withdrawal.

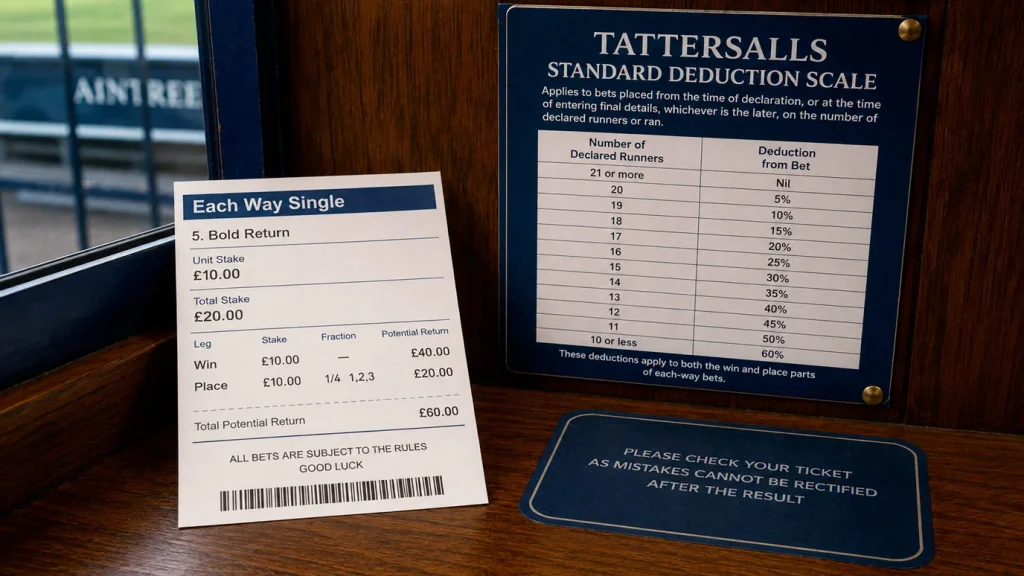

The Tattersalls deduction scale

The full deduction scale is the heart of any Rule 4 conversation. It is worth knowing the rough bands because they tell you, before you place a bet, how exposed you are to a late withdrawal.

From 30/100 (3 to 10 on) or shorter, the deduction is 90p in the pound. From 2/5 to 8/15, it is 85p. From 4/9 to 4/7, 80p. From 8/15 to 4/6, 75p. From 8/13 to 4/5, 70p. From 5/6 to 4/5, 65p. From evens to 6/5, the deduction is typically 55p-50p. From 5/4 to 6/4, around 40p. From 13/8 to 9/4, 30p. From 5/2 to 3/1, 25p. From 100/30 to 4/1, 20p. From 9/2 to 11/2, 15p. From 6/1 to 9/1, 10p. From 10/1 to 14/1, 5p. From 16/1 to 22/1, nothing on most scales, with some operators applying a 5p deduction up to 19/1.

The pattern is clear once you see it written out. Withdrawn favourites trigger heavy deductions because their withdrawal shortens the rest of the market substantially; withdrawn outsiders trigger no deduction because their absence barely changes the market shape. A withdrawn 25/1 outsider in a 20-runner handicap leaves the rest of the field at almost the same prices. A withdrawn evens favourite in a six-runner field redistributes its 50% market share across the rest, and the bookmaker has to claw back the implied price shortening from settled bets to avoid a structural loss on the race.

The 2.7% rise in Premier Fixture turnover per race in 2025, against an 8.6% fall on Core Fixtures, told the BHA that high-profile cards are now where most betting money goes. The same data tells me that Rule 4 deductions on Premier Fixture races now move bigger absolute pound figures than they used to. A 25p in the pound deduction on a Saturday handicap at York is a different size of bite than the same deduction on a Wednesday Core Fixture, because the volume of bets it applies to is so much larger.

Applied to win and place legs separately

This is the line where most punters lose track. Rule 4 applies to the win leg and the place leg of an each-way bet as if they were two separate winning bets. The same percentage comes off both. There is no special treatment for each-way slips; the place leg is just another winning settlement that the deduction scale acts on.

Take a £10 each-way bet on a 10/1 shot in a 16-runner handicap. Place terms: four places at 1/4 the odds. The horse wins. Before any deductions, the win leg returns £10 × 10 = £100 profit plus £10 stake = £110 from the win leg. The place leg at 2.5/1 returns £10 × 2.5 = £25 profit plus £10 stake = £35 from the place leg. Total return: £145.

Now apply a Rule 4 of 25p in the pound, triggered by a 5/2 favourite withdrawn on the morning of the race. The win leg’s profit is reduced by 25%: £100 profit becomes £75. The win leg returns £75 + £10 = £85. The place leg’s profit is similarly reduced by 25%: £25 profit becomes £18.75. The place leg returns £18.75 + £10 = £28.75. Total return: £113.75. The Rule 4 took £31.25 out of what would have been a £145 settlement. That is a 21.5% reduction on the net profit of the bet.

The standard place-terms structure published in operator rulebooks, including the bet365 each-way rules referenced across the industry, is silent on Rule 4 specifically because Rule 4 sits separately in the Rules of Betting. But the deduction stacks. If a race triggers two Rule 4s — a 4/1 horse withdrawn at 9am and a 6/1 horse withdrawn at 11am, before the off — the deductions are summed, and the total deduction is applied to both legs. Two Rule 4s of 20p and 10p sum to a 30p in the pound deduction. Both legs of any winning each-way slip take a 30% cut on profit.

One small mercy: stakes are never touched. The £10 win stake comes back in full on a winning win leg. The £10 place stake comes back in full on a winning place leg. The deduction is only on the profit element.

When Rule 4 is skipped: BOG, SP and NRNB races

There are three contexts in which Rule 4 does not apply, and they are the cleanest reason to know each of those three product features intimately. The first is bets settled at starting price (SP). The starting price is the price the official UK SP returners record at the off, after all late withdrawals have been absorbed into the rest of the market. So a Rule 4 deduction is not applied to SP bets — the price has already adjusted. If you take SP on an each-way slip, you accept whatever the price is at the off, and Rule 4 is built into that price rather than deducted from it. The trade-off, of course, is that you do not know the SP until the race goes off; you cannot bank a known price.

The second is best odds guaranteed bets where the SP returns shorter than your taken price. BOG promises you the bigger of your taken price or the SP, but Rule 4 still applies to the taken price element. The interaction is fiddly: if your taken price after Rule 4 is shorter than SP, you usually get SP without deduction. If your taken price after Rule 4 is longer than SP, you get the deducted taken price. Operators differ on the small print here, and the £766.7m UK remote horse racing GGY recorded by the Gambling Commission for April 2024 to March 2025 includes a lot of bets where this interaction came out one way or the other. For BOG mechanics on the win leg in detail, including how Rule 4 interacts with the BOG promise at SP, the BOG and each-way value breakdown walks the rule through worked examples.

The third is races where the withdrawn horse is non-runner-no-bet and the slip is ante-post. NRNB ante-post books are priced to absorb withdrawals already; Rule 4 does not apply to the price you took ante-post. Day-of-race bets on the same race after the morning declarations can still take a Rule 4 hit. Two different protections on the same race, applied to different slips.

Why was my each-way return cut after a horse was withdrawn?

Rule 4 applied. A horse withdrawn after the market opened triggers the Tattersalls deduction scale, which reduces your gross winnings on both win and place legs by a percentage tied to the withdrawn horse"s price.

Does Rule 4 ever apply twice in a single race?

Yes. If two horses are withdrawn separately before the off, both deductions are summed and applied to your gross winnings. A combined deduction over 90p in the pound is rare but possible if multiple short-priced runners are pulled.

Can a Rule 4 deduction take my place return below my stake?

No. Rule 4 is applied only to the profit portion of your settlement. Your stake is always returned in full on a winning bet, and the deduction cannot push the gross settlement below the stake.

Articles

Created by the "Racing Place Betting" editorial team.